Mera Ghar Mera Ashiana Loan Scheme 2025 by State Bank of Pakistan SBP

Owning a house is a dream for many families in Pakistan, but high land prices and expensive bank loans often make it very hard. To make this dream possible, the Government of Pakistan has introduced the Mera Ghar Mera Ashiana Loan Scheme 2025, which is supervised by the State Bank of Pakistan (SBP).

This loan scheme is designed especially for people who are buying or building a house for the first time. It helps low- and middle-income families by offering low markup rates, long repayment time, and small down payments. By the end of this guide, you will know everything about the scheme, from who can apply to how the payments work.

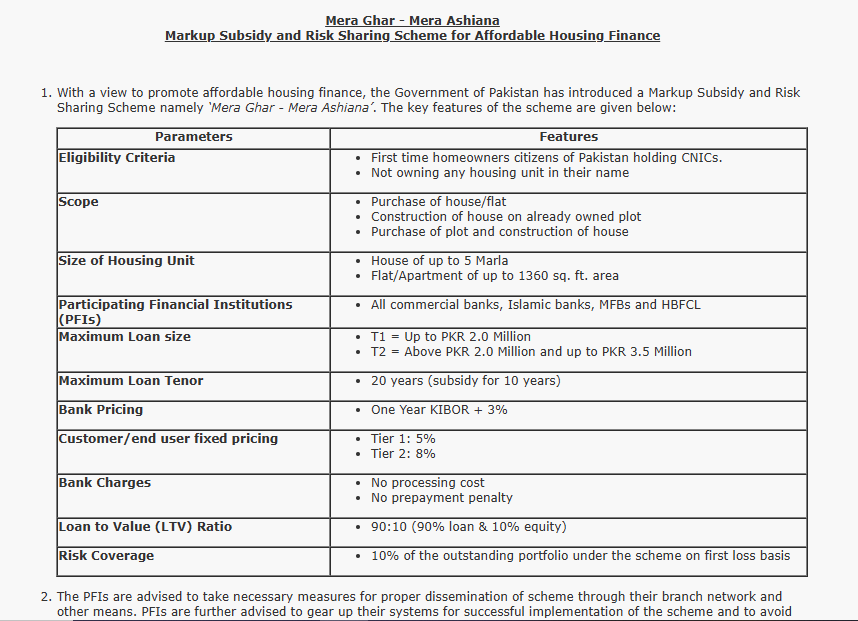

Who Can Apply?- Eligibility Criteria

The loan is only for people who are first-time home buyers. If you already own a house or flat, you cannot apply. The rules are:

- You must be a Pakistani citizen with a valid CNIC.

- You must not own any house, apartment, or property in your name.

- You must show income proof (salary slip, business record, etc.) to confirm you can repay the loan.

This means the scheme is focused on helping families who do not have their own home yet.

How to Apply for Mera Ghar Mera Ashiana Scheme

Here is the simple process to apply for the loan:

- Go to a participating bank branch with your CNIC.

- Ask for the Mera Ghar Mera Ashiana Loan form.

- Provide the required documents (CNIC, proof of income, salary slips, or business records).

- If you are buying or constructing, submit property papers.

- The bank will check your eligibility and loan size.

- Once approved, you will start your loan with monthly installments.

What the Loan Covers (Scope of the Scheme)

The Mera Ghar Mera Ashiana Scheme gives you different options. You can use the loan in these ways:

- Buy a ready-made house or flat.

- Build a house on your own plot.

- Buy a plot and build a house on it.

This flexibility makes the scheme useful for many people. Whether you want to buy or build, you can choose what fits your need.

House and Flat Size Limits

The government has fixed the maximum size for houses and flats so that only affordable homes are covered.

- House: Up to 5 Marla.

- Flat/Apartment: Up to 1,360 square feet.

This ensures that the scheme supports middle-class families, not luxury buyers.

Banks That Offer the Loan

The good thing about this scheme is that almost all commercial banks, Islamic banks, Microfinance Banks (MFBs), and House Building Finance Corporation (HBFCL) are part of it.

So, if you want to apply, you can simply visit your nearest major bank branch. The State Bank has ordered banks to guide people properly and make the process easy.

Loan Amount (Two Tiers)

The loan size is divided into two categories:

- Tier 1 (T1): Up to PKR 2 million.

- Tier 2 (T2): Above PKR 2 million and up to PKR 3.5 million.

This division makes sure that both small families and those needing slightly more money can get support.

Loan Time (Tenure)

The maximum loan time is 20 years.

- For the first 10 years, the government provides a markup subsidy.

- The long repayment time reduces the monthly installment, so families can manage it easily.

Markup Rates (Fixed and Affordable)

One of the biggest benefits of this scheme is the low fixed markup rate:

- Tier 1: 5% fixed.

- Tier 2: 8% fixed.

Normally banks charge much higher rates, but because of the government subsidy, you only pay this small markup. This makes it possible for more people to afford a home.

Loan to Value Ratio (Down Payment)

The Loan to Value (LTV) ratio is 90:10.

- 90% of the property value is given by the bank.

- You only pay 10% as down payment (equity).

This is a big relief for families who don’t have much savings.

Bank Charges

To keep things easy for the public, SBP has given special instructions:

- No processing fees.

- No penalty for early repayment.

So, if you want to clear your loan earlier, you can do it without extra charges.

Risk Coverage for Banks

The scheme also provides risk protection for banks. The government covers 10% of the loan portfolio as a first-loss guarantee.

This makes banks more confident to give loans to first-time home buyers.

Payment Example

Let’s understand how the payment works:

- If you take PKR 2 million for 20 years at 5%, your monthly installment will be much smaller than normal market loans.

- If you take PKR 3.5 million for 20 years at 8%, the installment is still affordable because of the subsidy.

In many cases, the monthly installment is almost equal to or less than the rent people usually pay.

Benefits of the Scheme

This loan program has many clear benefits:

- Very low markup (5% and 8%).

- Long repayment time (up to 20 years).

- Only 10% down payment required.

- No hidden bank charges.

- Loan available for both buying and building.

- Government risk cover to encourage more lending.

Role of SBP

The State Bank of Pakistan supervises the scheme. It ensures that banks follow the rules, help customers, and provide loans fairly. SBP also manages the subsidy and the risk-sharing with banks.

Why This Scheme is Important in 2025

With rising population and rapid urban growth, housing demand in Pakistan is higher than ever. Private loans are too expensive, and many families cannot afford them.

The Mera Ghar Mera Ashiana Loan Scheme 2025 is a strong step by the government to reduce this problem. By lowering markup and making repayment easier, it gives hope to thousands of families to finally own their dream home.

Conclusion

The Mera Ghar Mera Ashiana Loan Scheme 2025 is one of the best housing finance options in Pakistan. With affordable markup rates, long repayment options, small down payments, and wide bank participation, it is a golden chance for first-time buyers.

If you meet the eligibility conditions, this scheme can help you replace rent with easy monthly installments and finally become the owner of your own home.

For more details, you can check the official State Bank of Pakistan page: SBP Official Circular

Frequently Asked Questions FAQs

Q1: Can I apply if I already own a small house?

No, only first-time buyers can apply.

Q2: Which banks are offering this loan?

All commercial banks, Islamic banks, MFBs, and HBFCL.

Q3: Is there any penalty for early repayment?

No, you can repay anytime without penalty.

Q4: What is the size limit for houses and flats?

Houses up to 5 Marla and flats up to 1,360 sq. ft.

Q5: How much down payment do I need?

You only need 10% of the property value

One Comment